Strong Know Your Customer (KYC) onboarding measures are mandatory for regulated companies. But these measures needn’t get in the way of a seamless and relatively quick customer onboarding process. Delivering effective KYC and a positive user experience are possible and necessary for businesses that want to thrive in the new digital-first economy.

At first glance, it seems the security measures required for robust KYC and the simplicity of a quick sign-up are at odds with each other. On the one hand, KYC is about getting all the necessary information that compliance teams require to make an informed Customer Due Diligence decision. On the other hand, potent customer onboarding is about quickly and easily gathering enough data about a customer to begin serving them.

How can the customer onboarding process provide both a depth of information and a simple sign-up?

A Layered Approach to Customer Onboarding

Note some critical distinctions in the requirements; you need the necessary information to begin. You might not need to gather every available KYC data point, for every customer, right at the beginning.

Instead, a more nuanced approach that gathers enough information to enable onboarding allows the customer to start transacting without unnecessary friction. This risk-based approach considers factors such as:

- Jurisdictional requirements

- Industry

- Customer country

- Transaction volume and amount

- Other customer risk profile considerations

For example, many gaming companies regulated under KYC and Anti-Money Laundering (AML) laws use a layered approach to customer onboarding. A layered approach for onboarding is about balancing: It emphasizes collecting and verifying a user’s personally identifiable information (PII) without interrupting the customer journey. Instead of asking users for their identity attributes all at once, layered onboarding lets users follow their curiosities and explore the product, asking them for identity attributes as the customer relationship grows or at different thresholds of product engagement.

Many of the top crypto companies also use a layered approach to customer onboarding. In general, the first step is identity verification, which requires filling in basic identity information. Higher-value accounts may also require document verification.

AML/KYC Client Onboarding Regulations

The first criteria to consider when managing your AML/KYC customer onboarding process are the specific legal requirements. If not prescribed in legislation, many regulators will provide details on the demands or offer guidance on what procedures to follow. It’s important to understand these are the minimum needs for compliance. Many companies prefer to use global AML best practices to ensure robust, scalable and adaptable programs.

Understanding jurisdictional requirements will define what type of information you need to collect, how you can collect it and appropriate ways to analyze and review the authenticity and legitimacy of the data.

For an overview, consider the Customer Due Diligence recommendations from The Financial Action Task Force (FATF), an independent inter-governmental body. They recommend:

- Identifying the customer and verifying that customer’s identity using reliable, independent source documents, data or information

- Identifying the beneficial owner and taking reasonable measures to verify the beneficial owner’s identity so the financial institution is satisfied it knows who the beneficial owner is. For legal persons and arrangements, this should include financial institutions understanding the ownership and control structure of the customer

- Understanding and, as appropriate, obtaining information on the purpose and intended nature of the business relationship

- Conducting ongoing due diligence on the business relationship and scrutiny of transactions undertaken throughout that relationship to ensure the transactions being performed are consistent with the institution’s knowledge of the customer, their business and risk profile, including, where necessary, the source of funds

The first recommendation is about performing identity verification on individual customers, while the second recommendation concerns itself with verifying business customers. While additional due diligence measures are necessary, identity verification is essential for AML/KYC compliance.

As identity verification is a requirement, companies that can minimize friction at this stage while still delivering compliance have a crucial differentiator for their customer onboarding program.

The Need for Speed When Signing Up

According to an article in Finextra, 63% of banking customers have abandoned an online account creation process; the main reasons are that the onboarding process is taking too long or requires more information than they want to disclose.

A Trulioo commissioned Consumer Account Opening Report revealed that 73% of people consider the account opening process a “make or break” point in their future relationship with a brand. People have become used to quickly opening up accounts, and online success depends on matching that expectation.

While business customers might not have that same expectation when opening their business accounts, unfortunately, delays are much more pronounced in those situations. Another article in Finextra states it takes 3-4 months to onboard a corporate banking customer. The lengthy delays lead to application abandonment and, as a result, “in 2019, it was deduced that the global commercial and business banking market lost $3.3 trillion.” Correctly identifying business ownership is a compliance issue that also affects customer acquisition and bottom-line performance.

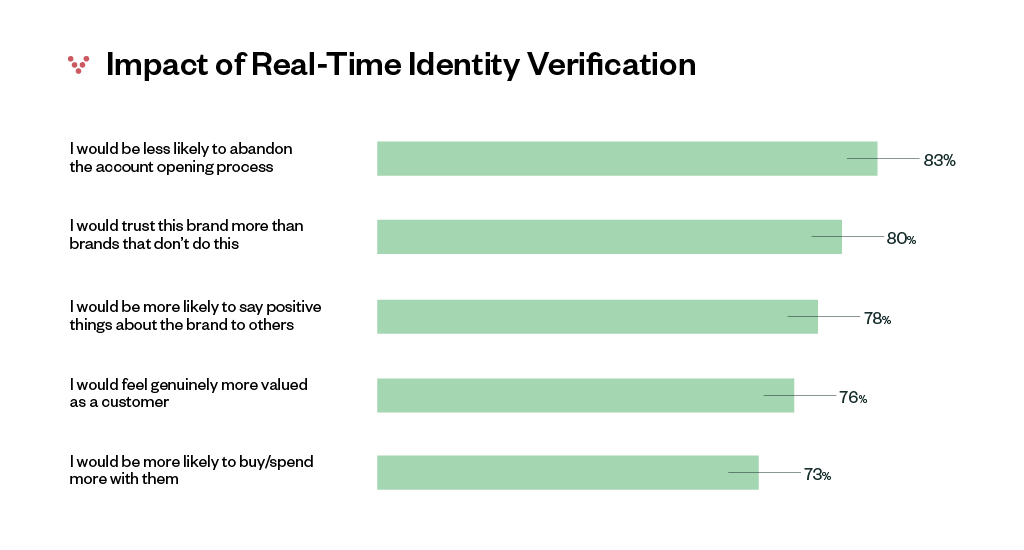

In either onboarding situation, speeding up the process results in more customers since the abandonment rate decreases. Additionally, a quick onboarding experience creates a positive impression of the brand and contributes to higher customer satisfaction. The Consumer Account Opening Report finds fast and secure account creation built around real-time identity verification results in significant improvements in brand and business outcomes:

The critical point is to deliver an initial onboarding experience that provides what the customer wants – getting an account without an undue amount of time or effort. Once they have an account, the customer can start using the service and decide if it’s right for them. If they like the service, they are much more accepting of providing further identity information if required. The key is to communicate the need to collect the data at some point and explain the need for enhanced security.

Every country, industry, business and customer are different; taking a layered approach can help ensure customer onboarding is as fast as possible without compromising compliance or fraud prevention measures. With advanced identity verification technology, customer onboarding that delivers KYC and AML compliance and a pleasant user experience is achievable.

Solutions

Customer Onboarding

Achieve Agile Customer Verification Around the World

Featured Blog Posts

Business Verification (KYB)

Enhanced Due Diligence Procedures for High-Risk CustomersIdentity Verification

Proof of Address — Quickly and Accurately Verify AddressesBusiness Verification (KYB)

How to Verify Legitimate Businesses and Merchants